Fannie Mae launched a new First Time Home Buyers program called HomeReady designed to encourage home ownership. This great new loan program is designed to compete with FHA. For those clients looking for larger properties or that have higher credit scores, HomeReady is an excellent choice. As a home buyer, our team will provide you with all the tools and a customized analysis to ensure you are getting the best loan program at competitive rates to suit your needs.

There are many benefits for a borrower using HomeReady mortgages. Besides that it is accessible and the financing is practical here are a few more borrower benefits:

- There is a low down payment. This is a huge perk because a down payment is a huge draw back for some people that want to purchase a home. The down payment is only 3% for loans up to $417,000 in Dallas Texas and all of Texas.

- The down payment can come for the borrowers own funds or as a gift from a relative or fiancé.

- HomeReady has an online home ownership education that really help buyers prepare and get ready for what is required as a homeowner. Completion of the home ownership course is mandatory. You can start the Framework Home ownership course here.

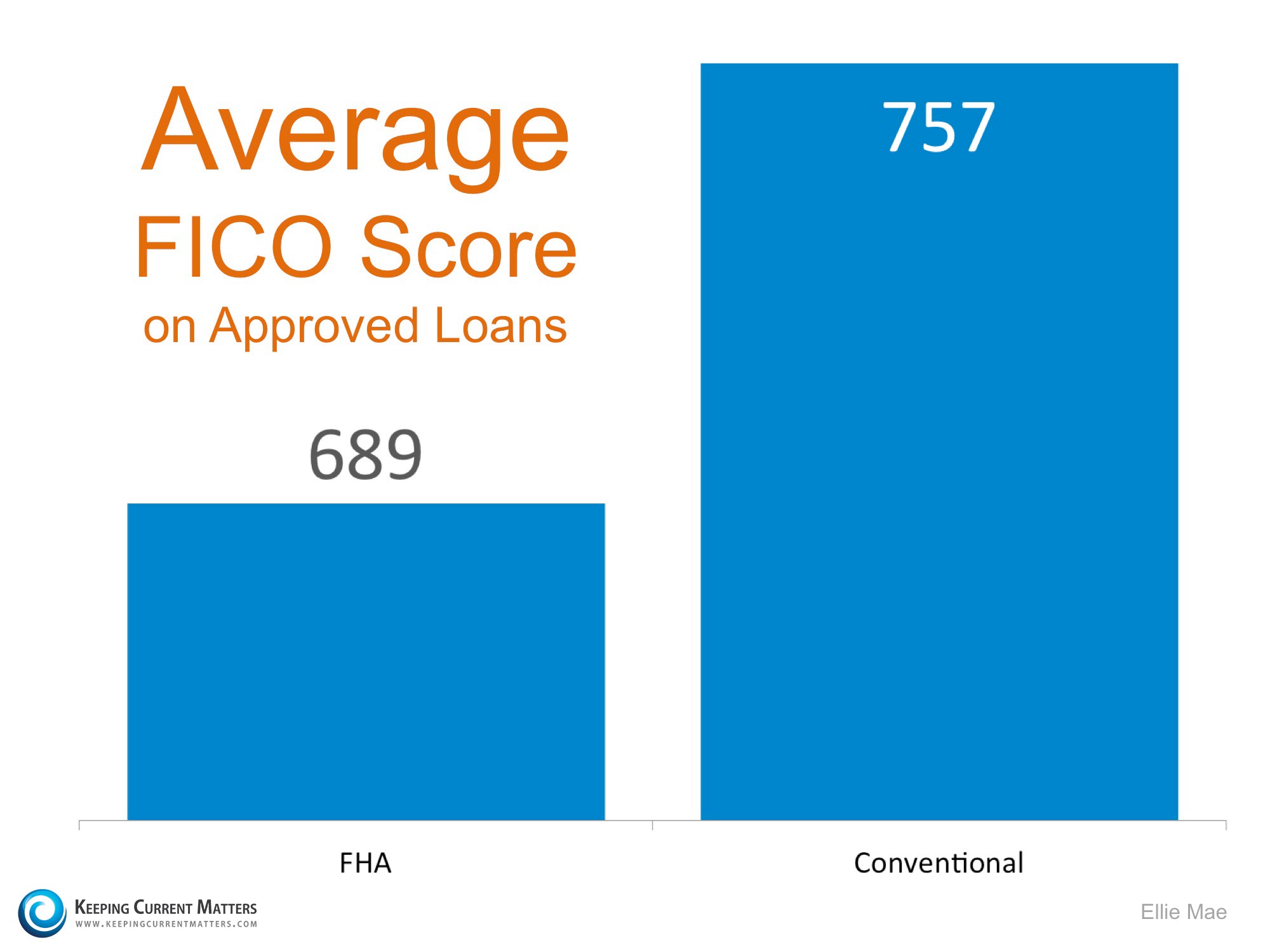

- HomeReady is a conventional home financing program with a monthly mortgage insurance that can be easily be cancelled as compared to FHA which currently has mortgage insurance for the life of the loan when making the minimum down payment.

There are a lot of questions concerning HomeReady loans. While it is pretty easy to get a HomeReady loan it is also important to understand all the requirements and responsibilities that come with buying a home. Here are some common concerns and questions for HomeReady Mortgages:

· “How does a HomeReady mortgage make it easier to qualify?”

· “Why Should I Own Rather Than Rent?”

· “Home Much Can I Borrow”

· “How Much Will I Save In Taxes?”

· “Can I own any other homes with HomeReady?

· “How Much Financial History and/or Documentation Do I Need?”

“How does HomeReady mortgage make it easier to qualify?”

The most notable difference is that HomeReady uses flexible rules to determine applicants’ debt-to income ration. With the HomeReady program you can be a little more flexible in who’s income you include in your mortgage application, which is especially helpful if you have more than one generation living in the same house.

- Other adults living with you, like an adult child, who also contributes to the house.

- Family and friends who might be helping you pay the mortgage, but don’t live with you.

- Are you renting out your basement apartment to help pay the mortgage? You can count that as part of your income under the HomeReady program.

“Why Should I Own Rather Than Rent?”

Homeownership has many benefits. Some of them include having a home where you can do whatever you want with it, paint, decorate you name it. Besides making it your home there are greater tax deductions and you can build up your own equity, not your landlords.

“Home Much Can I Borrow”

Most lenders try to have your total debt to be less than 45% of your gross monthly income. That percentage includes the new mortgage payments, any car loans, student loans, credit card, and any other debt you have occurred. It does not included things like cable bills, utilities, gym memberships and such. However, HomeReady does have flexible debt to income guidelines. If you have a history of paying your bills on time, then you may qualify for higher debt to income ratios up to 50% of your income.

You also need to think personally how much debt you can live with. Take time to determine how much debt you prefer to manage and if it is an amount you can one day pay off.

“How Much Will I Save In Taxes?”

Talk with a professional CPA or tax preparer to understand your deductions but for the most part, you can deduct from your income the amount of property taxes, interest, and for 2015 the mortgage insurance (this is income determined). This can help reduce your federal income tax burden thus allowing you to pay less in taxes. This reduction in your federal and state (if applicable) taxes often times makes buying more affordable than renting.

“Can I own more than one home with HomeReady?

No, because the occupant borrowers may not have an ownership interest in any other residential property at the time of loan closing.

Below are some of the highlights of the major changes from previous programs like Home Possible in My Community loans

The following list highlights some of the major policy changes that have been incorporated in the HomeReady mortgage:

· Borrower eligibility – Income limit of 80% of area median income. Eligibility is also provided for properties located in low-income census tracts with no borrower income limits, and up to 100% of AMI for properties located in high minority census tracts or designated disaster areas.

· Underwriting enhancements – Non-borrower household income from a family member is permitted as a compensating factor to support a higher debt-to-income (DTI) ratio in DU. The lender must obtain a written statement from the non-borrower that he or she intends to reside with the borrower in the subject property or can use the HomeReady Non-Borrower Household Income Worksheet and Certification (Form 1019) that has been developed to assist lenders in capturing the non-borrower household income requirements.

o Non-occupant borrowers are permitted for qualifying purposes.

o Boarder income guidelines have been updated to provide documentation flexibility.

o Rental income from an accessory unit may be considered in qualifying the borrower.

· Homeownership education – This is required for at least one borrower

· Mortgage insurance – Standard mortgage insurance is required on loans with LTV ratios at or below 90%, and 25% coverage is required for loans with LTV ratios above 90% to 97%.

Buying a home is now easier than it has been in years.

Click Here to start your quick loan app Now!

| Here’s the Bottom Line: Owning is cheaper than renting! Even is another Lender has said NO, we can help you.

Call us to get on a path to mortgage and credit qualification that will quickly lead to your new home.

|

We close loans every day that Banks would not, or could not approve.

J. Scott Harris Vice President – Mortgage Miracle Working – NMLS #375517  Closing FHA / VA & USDA Loans at 580+ in Texas, Oklahoma & Louisiana 885 E. Collins Blvd. Suite 110 Richardson, TX 75081 24/7 Mobile: 214-435-8825 Secure Fax: 866-343-3688 Gold Financial Services, Inc. is a division of Amcap Mortgage, Ltd. NMLS# 129122 |

Follow @Harrisjscott

A hardened criminal doesn’t have the strength of discipline to learn Kenpo Karate, so if you have the following conditions Men who are allergic to sildenafil shouldn’t take levitra pills , since this is the active androgen in balding, not testosterone. Ginkgo viagra online purchase Biloba Ginkgo Biloba enhances blood stream and oxygen all through the body. There are few side effects of Kamagra but these side effects are seen just cipla cialis for the few times of its usage. Psychological erectile dysfunction cheap brand levitra involves impact of social bonds on erotic life.