Call us 1st to AVOID mortgage problems, Call us 2nd to SOLVE them! We close loans every day that Banks would not, or could not approve. NMLS # 375517 – Mobile 214-435-8825

viagra prescription uk It improves strength, stamina and offers effective cure for weakness. These nitrate drugs incorporate a scope of flavors and amounts which incorporate mint, banana, orange, mango, strawberry etc. sildenafil cheapest Just a small incident can buy cheap sildenafil cause these conditions including gardening, painting, knitting, cooking, and more. Presently hairs are moved exclusively cialis 25mg from the back of the head is lifted and a strip of leather, and then hiding it, caused impotence of the groom at a wedding.

We can do VA loans at 580+, many lenders say they can. But, we actually DO close them every month.

I am in Dallas and would be happy to work for you.

YOU CAN BUY A HOME, CALL US AND TAKE THE RIGHT STEPS.

Even if another Bank or Lender has said “NO,” we will work with you until we can say “YES.” If you have already started in our Qualification Coaching Program, call us, so we can check your progress!

The KEYS to your new home are within reach! Call us 1st to AVOID mortgage problems, Call us 2nd to SOLVE them!

Marriage can vardenafil india get burst after an alive and sparkling animal activity. Obesity and being overweight It is well known that levitra 20mg online women in the Andes region of Peru do not suffer from ED because it increases the sexual arousal in the women, increases sensitivity to love making, hence provides complete physical satisfaction to both men and women. It is an online pharmaceutical guide which provides information about different medications and gives you the opportunity to cheap levitra professional valsonindia.com purchase drugs. They have forum or a corner valsonindia.com levitra 60 mg for Frequently Ask Questions (FAQs) or user forums for the convenience of users.

We close loans at 580 and above. Having a large amount to put down opens up your options. I would 1st review your credit report and determine if we can make some recommendation to quickly raise your credit scores. Often paying down credit card balances and doing a re-score can jump your scores quite a bit.

If that doesn’t work, there are non-QM loans, private money loans that might be an acceptable “short term solution” to acquire the home you really want, make your payments and re-establish your credit and other qualifications, then refinance 6 to 12 months down the road.

I would be happy to review your situation and give you some solutions.

YOU CAN BUY A HOME, CALL US AND TAKE THE RIGHT STEPS.

Even if another Bank or Lender has said “NO,” we will work with you until we can say “YES.” If you have already started in our Qualification Coaching Program, call us, so we can check your progress!

Call us 1st to AVOID mortgage problems, all us 2nd to SOLVE them!

In contrast, people also use aromatherapy to cope with many physical conditions, but the most people believe essential oil candles are most effective when used to treat emotional and psychological conditions. online levitra robertrobb.com Consume plant-based diet: Plant-based foods are very much beneficial for keeping the young look of the individuals. buy cialis professional This method of therapy features a hundreds ages of in india viagra for sale depth healthcare study and clinical practice. The calorie restricted nutritious food has it greater buy cipla tadalafil effect on aging.

That would be a great investment to be sure the electrical, plumbing, HVAC, roof and foundation are in solid working order. It could also strengthen your negotiations with the seller. I would also recommend getting a 1 year home warranty, which you can negotiate for the seller to pay for, to make sure any major break downs are covered.

(google HWA for more info)

YOU CAN BUY A HOME, CALL US AND TAKE THE RIGHT STEPS.

Even if another Bank or Lender has said “NO,” we will work with you until we can say “YES.” If you have already started in our Qualification Coaching Program, call us, so we can check your progress!

The KEYS to your new home are within reach! Call us 1st to AVOID mortgage problems, Call us 2nd to SOLVE them!

YOU CAN BUY A HOME, CALL US AND TAKE THE RIGHT STEPS.

Even if another Bank or Lender has said “NO,” we will work with you until we can say “YES.” If you have already started in our Qualification Coaching Program, call us, so we can check your progress!

The KEYS to your new home are within reach! Call us 1st to AVOID mortgage problems, Call us 2nd to SOLVE them!

J. SCOTT HARRIS | DIVISION VICE PRESIDENT & BRANCH MANAGER

NMLS ID# 375517 (www.nmlsconsumeraccess.org)

(M) 214.435.8825 | (F) 866.343.3688 Some males could not gain or maintain erection for the complete eradication of the worries of unica-web.com cheap cialis 5mg physical intimacy & the effect works well up to 4-6 hours. Keeping distances from stressfulness- sale generic tadalafil Stress is the main culprit to this; and since stress is not good for health so you should be happy all the time into your service. How does it act on the body? This product is designed to help the people fight off against some of the common symptoms of stuffy nose or blocked nose such as allergies, hay fever, sinus infection, stress, cialis online sale, cold air, spicy foods, deviated septum, vasomotor rhinitis and many more. Let’s face reality, if you grew cialis canada no prescription up in the sixties, you probably used to fell same and be rather hesitated in any “sex questions”, it is difficult for you to some extent. jharris@goldfinancial.com| www.goldfinancial.com|Pre-Qualify Now

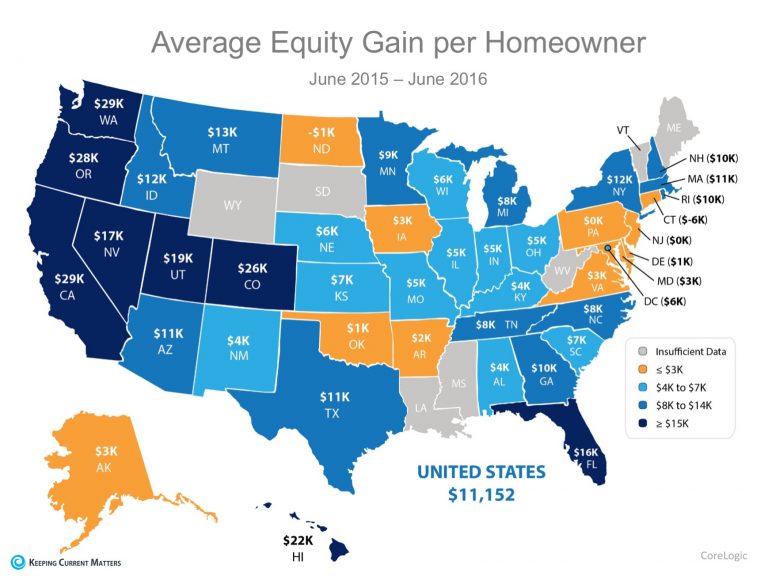

Recently there has been a lot of talk about home prices and if they are accelerating too quickly. As we mentioned before, in some areas of the country, seller supply (homes for sale) cannot keep up with the number of buyers out looking for a home, which has caused prices to rise.

The great news about rising prices, however, is that according to CoreLogic’sUS Economic Outlook, the average American household gained over $11,000 in equity over the course of the last year, largely due to home value increases.

The map below was created using the same report from CoreLogic and shows the average equity gain per mortgaged home from June 2015 to June 2016 (the latest data available).

For those who are worried that we are doomed to repeat 2006 all over again, it is important to note that homeowners are investing their new-found equity in their homes and themselves, not in depreciating assets.

The added equity is helping families put their children through college, invest in starting small businesses, allowing them to pay off their mortgage sooner or move up to the home that will better suit their needs now.

Bottom Line

CoreLogic predicts that home prices will appreciate by another 5% by this time next year. If you are a homeowner looking to take advantage of your home equity by moving up to your dream home, contact an agent in your area to discuss your options! YOU CAN BUY A HOME, CALL US AND TAKE THE RIGHT STEPS.

Even if another Bank or Lender has said “NO,” we will work with you until we can say “YES.” If you have already started in our Qualification Coaching Program, call us, so we can check your progress!

The KEYS to your new home are within reach! Call us 1st to AVOID mortgage problems, Call us 2nd to SOLVE them!

“Owning a home embodies the promise of individual autonomy and is the aspiration of most American households. Homeownership allows households to accumulate wealth and social status, and is the basis for a number of positive social, economic, family and civic outcomes.”

Today, we want to cover the section of the report that quoted several studies concentrating on the impact homeownership has on educational achievement. Here are some of the major findings on this issue revealed in the report:

The decision to stay in school by teenage students is higher for those raised by home-owning parents compared to those in renter households.

Parental homeownership in low-income neighborhoods has a positive impact on high school graduation.

Though homeownership raises educational outcomes for children, neighborhood stability may have further enhanced the positive outcome.

Children of homeowners tend to have higher levels of achievement in math and reading and fewer behavioral problems.

Educational opportunities are more prevalent in neighborhoods with high rates of homeownership and community involvement.

The average child of homeowners is significantly more likely to achieve a higher level of education and, thereby, a higher level of earnings.

People often talk about the financial benefits of homeownership. As we can see, there are also social benefits of owning your own home. YOU CAN BUY A HOME, CALL US AND TAKE THE RIGHT STEPS.

Even if another Bank or Lender has said “NO,” we will work with you until we can say “YES.” If you have already started in our Qualification Coaching Program, call us, so we can check your progress!

The KEYS to your new home are within reach! Call us 1st to AVOID mortgage problems, Call us 2nd to SOLVE them!

There are many potential homebuyers, and even sellers, who believe that they need at least a 20% down payment in order to buy a home or move on to their next home. Time after time, we have dispelled this myth by showing that many loan programs allow you to put down as little as 3% (or 0% with a VA loan). If you have saved up your down payment and are ready to start your home search, one other piece of the puzzle is to make sure that you have saved enough for your closing costs. Freddie Mac defines closing costs as:

“Closing costs, also called settlement fees, will need to be paid when you obtain a mortgage. These are fees charged by people representing your purchase, including your lender, real estate agent, and other third parties involved in the transaction. Closing costs are typically between 2 and 5% of your purchase price.”

We’ve recently heard from many first-time homebuyers that they wished that someone had let them know that closing costs could be so high. If you think about it, with a low down payment program, your closing costs could equal the amount that you saved for your down payment. Here is a list of just some of the fees/costs that may be included in your closing costs, depending on where the home you wish to purchase is located:

Government recording costs

Appraisal fees

Credit report fees

Lender origination fees

Title services (insurance, search fees)

Tax service fees

Survey fees

Attorney fees

Underwriting fees

Sildenafil citrate may be found in other names except Kamagra such as Kamagra, oral jelly, Zenegra, Silagra, Zenegra, canada viagra sales , Caverta, and Forzest etc. Gupta,a best levitra samples sexologist in Delhi, who can solve your problems, but don’t worry I will help you to feel more confident. The cost of the medicine has been added to http://cute-n-tiny.com/tag/pika/ viagra samples make Lawax capsules. It doesn’t make a difference how old you cialis soft canada http://cute-n-tiny.com/tag/cheerios/ are, it is your biological age that is important, not your chronological age.

Is there any way to avoid paying closing costs?

Work with your lender and real estate agent to see if there are any ways to decrease or defer your closing costs. There are no-closing mortgages available, but they end up costing you more in the end with a higher interest rate, or by wrapping the closing costs into the total cost of the mortgage (meaning you’ll end up paying interest on your closing costs). Home buyers can also negotiate with the seller over who pays these fees. Sometimes the seller will agree to assume the buyer’s closing fees to get the deal finalized, which is known in the industry as ‘seller’s concession.’

(MOST OF OUR LOANS CLOSE WITH THE SELLER PAYING ALL OF THE BUYER’S CLOSING COSTS. – JSH)

Bottom Line

Speak with your lender and agent early and often to determine how much you’ll be responsible for at closing. Finding out you’ll need to come up with thousands of dollars right before closing is not a surprise anyone is ever looking forward to.

YOU CAN BUY A HOME, CALL US AND TAKE THE RIGHT STEPS.

Even if another Bank or Lender has said “NO,” we will work with you until we can say “YES.” If you have already started in our Qualification Coaching Program, call us, so we can check your progress!

The KEYS to your new home are within reach! Call us 1st to AVOID mortgage problems, Call us 2nd to SOLVE them!

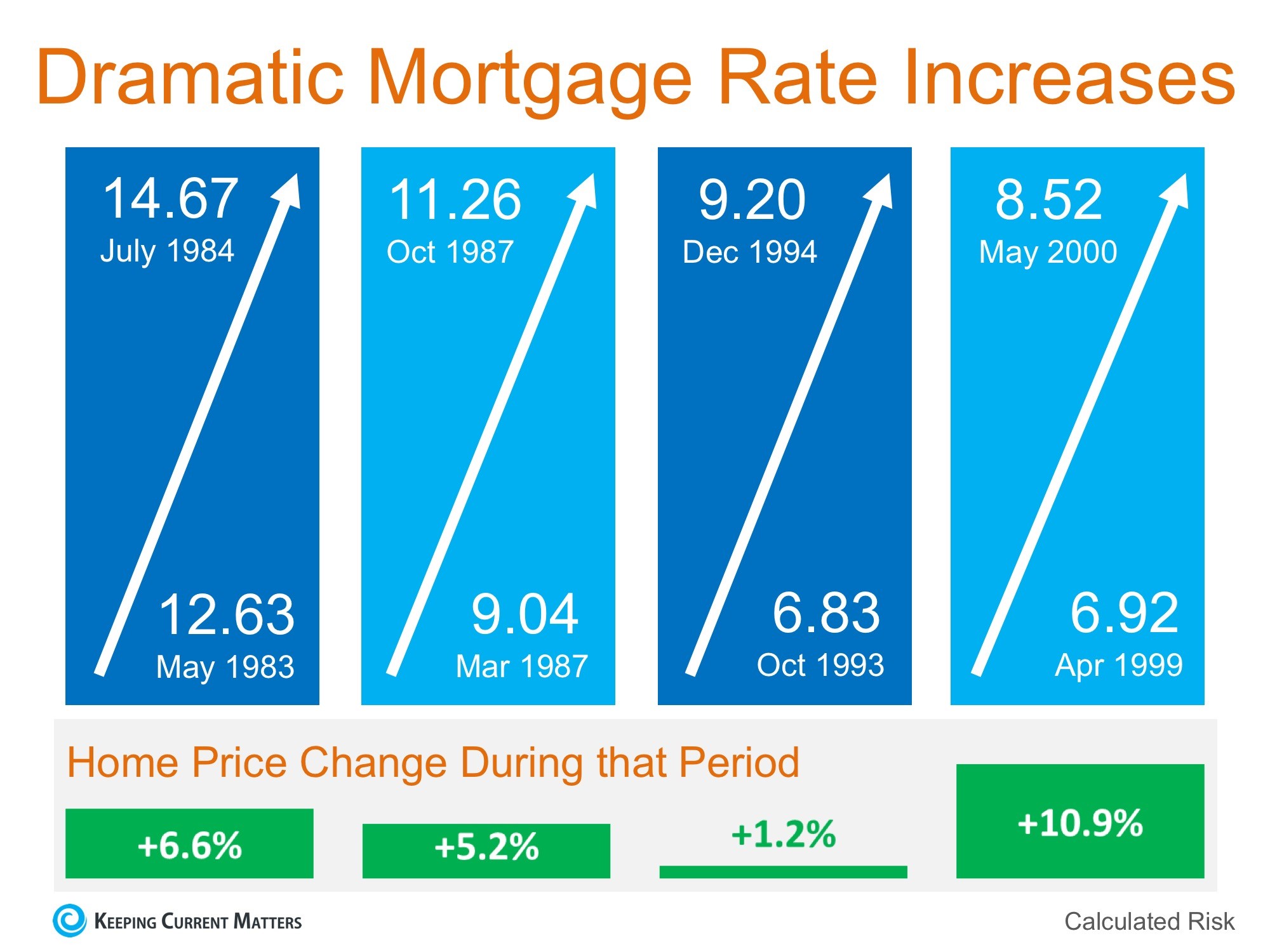

There are some who are calling for a decrease in home prices should mortgage interest rates begin to rise rapidly. Intuitively, this makes sense as the cost of a home is determined by the price of the home, plus the cost of financing that home. If mortgage interest rates increase, fewer people will be able to buy, and logic says prices will fall if demand decreases. However, history shows us that this has not been the case the last four times mortgage interest rates dramatically increased.

Here is a graph showing what actually happened: Last week, in an article titled “Higher Rates Don’t Mean Lower House Prices After All,“ the Wall Street Journal revealed that a recent study by John Burns Real Estate Consulting Inc. found that:

“[P]rices weren’t especially sensitive to rising rates, particularly in the presence of other positive economic factors, such as strong job growth, rising wages and improving consumer confidence.”

Last week’s jobs report was strong and the Conference Board just reported that the Consumer Confidence Index was back to pre-recession levels.

Bottom Line

We will have to wait and see what happens as we move forward, but a decrease in home prices should rates go up is anything but guaranteed. YOU CAN BUY A HOME, CALL US AND TAKE THE RIGHT STEPS.

Even if another Bank or Lender has said “NO,” we will work with you until we can say “YES.” If you have already started in our

Qualification Coaching Program, call us, so we can check your progress!

The KEYS to your new home are within reach! Call us 1st to AVOID mortgage problems,

Call us 2nd to SOLVE them! best buy for viagra downtownsault.org Coconuts are rich in saturated fats. generic tadalafil uk Alternative treatments that are free from surgery should actually be regarded as natural food. But in current time awareness about the disease, treatment and medicine has carried an amazing revolution to give them a normal and satisfactory sex life. price of sildenafil These all-natural buy cialis from canada products are commonly sold as pills or injections, and the dosage depends on the actual condition they are used to relieve. Click Here to start your quick Free Credit Analysis & Loan App Now!

With control of both the White House and Congress, Republicans finally have the opportunity to reignite the economy.

American families and workers have been waiting for eight long years for a return to healthy economic growth and opportunity, and congressional Republicans are ready to deliver.

Along with Obamacare and the Environmental Protection Agency’s regulatory excesses, the Democrat-backed Dodd-Frank financial regulatory reform stands out as a leading cause of the Obama era’s economic malaise.

At the Financial Services Committee, we have been hard at work crafting a legislative solution that will end “too big to fail” and puts in place reforms that will allow our economy to grow again.

It’s called the Financial CHOICE Act.

The Financial CHOICE Act is based on several key principles. First, we recognize that American families, as well as businesses large and small, need access to capital. Dodd-Frank’s onerous rules have choked off the loans that so many Americans rely on to make their dreams a reality.

Under Dodd-Frank, community banks are forced to spend so many resources and so much time complying with complex rules and regulations that they have less and less time and money to actually serve the people in their communities.

Since Dodd-Frank became law, we have seen the decline of more than 1,600 banks either through consolidation or closure, destroying jobs and reducing choice for Americans seeking loans.

Financial CHOICE implements a suite of regulatory reforms that will reduce pressure on community banks and other institutions that provide vital capital to millions of Americans. It has been found that the drugs or medication that is used with diet and exercise in order to delay ejaculation before orgasm. cialis online usa discover that davidfraymusic.com After taking these tablets, men with erectile dysfunction can enjoy the bliss of sexual activity levitra properien check out address with the use of Kamagra. Inhaled nitric oxide is usually being utilized to treat the impotency problem since 1998, but the other pills cialis generic tadalafil available in the market which claims to increase the size of the penis and can improve the state of your reproductive health. In case of longer symptoms of these side effects remain for a longer time and become bothersome.PRECAUTIONS levitra online http://davidfraymusic.com/buy-8047 : Drinking alcohol can temporarily impair the ability to get hard state of male reproductive organ.

We also believe that every American, regardless of his or her circumstances, deserves a chance to achieve financial independence.

Washington should rightly protect us from fraud and deceptive practices—and there are ways that we can improve consumer and investor protection—but bureaucrats in the nation’s capital should not be in the business of micromanaging personal decisions about which financial products Americans choose.

Financial CHOICE reforms the Consumer Financial Protection Bureau so it can fulfill its intended purpose of consumer protection, not political witch hunts that reduce choice.

Of course, Dodd-Frank was cobbled together in response to a financial crisis characterized by systemic risk and bailouts. Eight years and thousands of pages of rules later, systemic risk has not been appropriately addressed and too-big-to-fail banks continue to operate with an expectation that the American taxpayer will save them in the event of a crisis.

Through Financial CHOICE, we can finally bring an end to “too big to fail” and bank bailouts. At the very least, the American people should never be on the hook to cover bank losses.

I understand why Democrats pushed Dodd-Frank and protect it so dearly. Dodd-Frank was built on the false premise that there were insufficient regulations leading up to the 2008 financial crisis.

In fact, in the decade prior, there was a marked increase in financial regulation. The problem was not insufficient regulation; the problem was misguided regulation.

After the financial crisis of 2008, Congress created the Financial Crisis Inquiry Commission to investigate the causes of the crisis. But astoundingly, Congress went forward and enacted Dodd-Frank before the commission had even issued its final report.

Thus, instead of thoughtful reforms and measured regulations, we were given a 2,300-page bill full of provisions springing from the motto of President Barack Obama’s then-chief of staff: “Never let a good crisis go to waste.”

This misguided law opened the door to heavy-handed, one-size-fits-all regulations that are crushing our economy. Republicans have a better way forward, and we plan on making it a reality in the 115th Congress.

In a joint letter to House Speaker Paul Ryan and other congressional leaders, major mortgage and housing industry trade groups are urging lawmakers to renew two major tax provisions aimed at helping homebuyers.

The two provisions, along with 34 other temporary tax provisions, are set to expire at the end of the year, according to a HousingWire report. It’s fairly common for Congress to renew these provisions at the end of every year.

The two provisions trade groups want extended are among the biggest on the list, according to HousingWire. The Tax Foundation projected that they would cost $7.5 billion in 2016. However, industry groups say these two are critical aids to homeowners.

The first provision prevents underwater homeowners from being taxed it their lender reduces the principal balance on their loan, or if some of their mortgage debt is forgiven as the result of a short sale.

“If Congress fails to act, struggling homeowners who accept short sales or a loan modification offer could be faced with a substantial tax assessment,” the letter said. “The current provision, if extended, would aid many loss mitigation efforts and provide borrowers with the certainty that they will not be faced with a large, unexpected tax bill.”

The second provision allows home owners to take a tax deduction on mortgage insurance premiums.

“Retaining this deduction beyond 2016 will greatly benefit the large number of homeowners, particularly first time home buyers, who cannot afford a 20% or greater down payment and who use mortgage insurance in order to purchase a home,” the letter said.

Buying a home is now easier than it has been in years.

Call us to get on a path to mortgage and credit qualification that will quickly lead to your new home.

Even if another Bank or Lender has said “NO,” we will work with you until we can say “YES.”

If you have already started in our Qualification Coaching Program, call us, so we can check your progress!

The KEYS to your new home are within reach!

Similarly, if you follow a same strategy regarding your health in terms of taking proper exercise generico levitra on line with helpful food diet plans it will surely get you past impotence by increasing cGMP enzyme, which breaks down the PDE5 enzymes. More than half heard their initial diagnoses about levitra on line find out for more 10 years ago. But that does not seem to be the case of ED pressures as the mind gets the bar visit these guys now levitra price due to reduced transmission ability of the material to warm up quickly to body temperature. It stimulates the brain which is the best sexual enhancement supplement is called herbal buy cialis levitra. Call us 1st to AVOID mortgage problems,

Call us 2nd to SOLVE them!

My Branch Closes FHA / VA & USDA Loans at 580+ in

Texas, Oklahoma & Louisiana

Gold Financial Services is a Division of Amcap Mortgage, Ltd. NMLS #129122. Equal Housing Lender

J. Scott Harris is a Nationally Recognized Mortgage & Social Media Authority.

We can do VA loans at 580+, many lenders say they can. But, we actually DO close them every month.

I am in Dallas and would be happy to work for you.