The quintessential American dream may include graduating college, getting a job and eventually buying a home.

However, the increasing cost of student loan debt may be altering that trajectory for many millennials.

Rather than purchase a house in their mid-to-late 20s or early 30s, the younger generation is waiting to jump into homeownership. Is this trend because recent graduates have too much debt already? Or, is the housing market slowing due to other factors? Rent.com investigates:

Approved and Denied

According to the Wall Street Journal and data from LoanDepot, a non-bank lending firm, student loan debt doesn’t immediately seem to affect whether or not a person is approved for a mortgage loan. In fact, of the nearly 46,000 first-time home buyers who sought mortgages LoanDepot tracked, about 75 percent were approved.

Both those who were funded and those who weren’t were comprised of a nearly equivalent amount of people who held student loans. For instance, 27.3 percent of people whose loans were approved had student debt while 26 percent of those denied had student loans. Based on those numbers, having school debt did not affect whether or not a person was awarded a mortgage.

The Size of One’s Debt

LoanDepot data did indicate some loan-approval impact as a result of student debt, however. A borrower’s ability to repay a loan can influence whether or not he or she will be approved for a new loan.

The amount of debt a person has and his or her income will determine loan qualification. If, say, a person only pays 3 percent of his or her income toward a student loan, he or she likely has the money to also afford a mortgage. Conversely, if a person pays 43 percent of his or her income toward student debt, he or she is at risk of being denied.

Increased Debt Means Decreased Loans

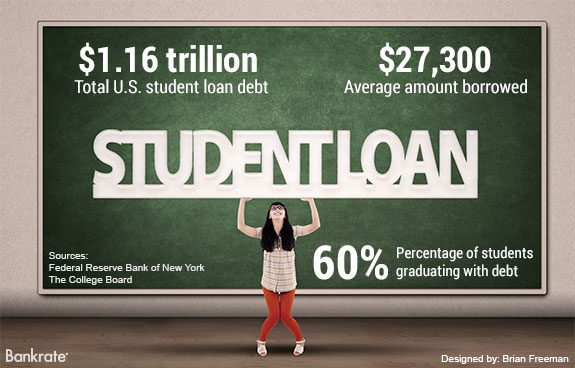

According to the Federal Reserve Bank of New York, the average sum a student repays at the end of his or her education is increasing. In 2003, most graduates left with a loan (or several loans from different sources) that was between $10,000 and $15,000. But in 2012, that average increased to between $20,000 and $22,000. People whose debt is significantly lower or higher remain outliers.

That means that the average graduate has more debt than those who graduated years prior. Not surprisingly, this increased debt may have translated to fewer millennials purchasing homes (though the relationship is more of a correlation than a causation). According to Harvard University’s Joint Center for Housing Studies, homeownership among millennials in the 25-34 age group has decreased by eight percentage points between 2004 and 2013.

Still, if graduates are able to land a high-paying job, they can afford their student loan and homeownership costs. The big X factor in a decreased housing market could be the tight economy and lack of well-paying positions.

Changing the Status Quo

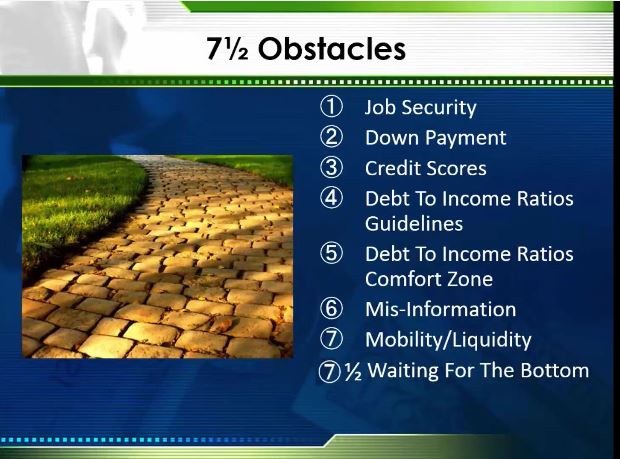

Because high monthly student loan payments may cause some lenders to deny potential homeowners, some in the industry have called for a change. Currently, lenders use credit scores and income date to generate an approved or denied status.

Rather than using the simple algorithm of comparing credit score and income, some industry experts suggest creating a new approval system that takes student loan debt into account – student borrowing isn’t likely to slow down anytime soon, as the cost of higher education has continued to increase. What a new system of borrowing would look like remains to be seen.

Reasons to Wait

While some people can’t get homeownership loans because they have been denied in the past, others simply don’t want to purchase a house. Some millennials choose to pay off their student debt, build their careers and settle down before making the move to homeownership.

What’s more, the average age of marriage is ever on the rise. According to U.S. Census data, men and women in 2010 waited to get married for the first time until they were in their late 20s. For this reason, millennials may hold off on buying a home.

Student debt, later marriage and low income all factor into whether or not millennials purchase a home in their mid 20s to mid 30s. Because the possible causes are numerous, it’s difficult to say what’s slowing the market.

More likely, all these elements have caused a decrease in homeownership among the younger population. Experts can really only provide correlations to shed light on the situation.

Original Article from Forbes.com